How to Open an Islamic Forex Account: The Forensic 2026 Compliance Onboarding Guide

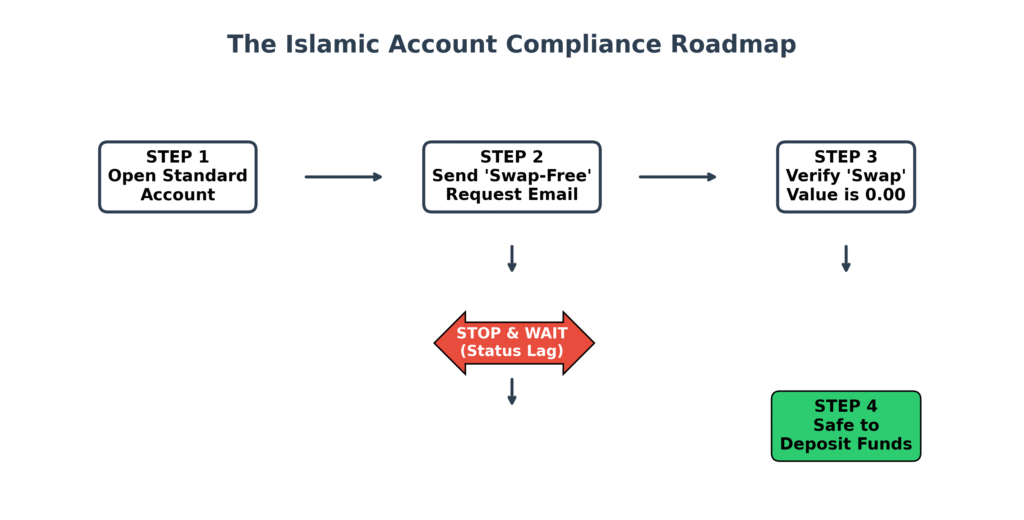

How do you open an Islamic Forex account correctly? To open a compliant Islamic Forex account, you must follow a 5-step forensic protocol: 1) Select a top-tier regulated broker with permanent swap-free status, 2) Register for a Standard account without funding it, 3) Manually trigger the “Compliance Change” by submitting a formal Swap-Free declaration to the support team, 4) Wait for written server-side confirmation, and 5) Verify the 0.00 swap parameters inside your MT4/MT5 terminal. This ensures you avoid the “Standard Trap” where interest accrues during the initial setup lag. Forensically, a valid onboarding must decouple the Tom-Next rollover from interest-bearing debt chains.

Learning how to open an Islamic Forex account correctly is your first line of defense against accidental Riba. While most beginners believe that “signing up” is just a simple administrative task, as an **ACCA-certified auditor** with 19 years of experience, I view it as a Contractual Transition. Opening a compliant account requires more than just ticking a box; it requires a forensic verification of the backend parameters that govern your money and the Shariah Governance of the institution. This guide serves as Part 13 of our Halal Trading Pillar Silo.

Key Takeaways: The Auditor’s Summary

- The Standard Trap: Almost all brokers require you to register an interest-bearing account first; trading during this “interim phase” is a major Riba risk.

- Manual Activation: Compliance often requires a specific Legal Declaration (Wakala Agreement) to be sent to the broker’s back-office to override default interest logic.

- Jurisdictional Audit: In 2026, accounts opened under Tier 1 regulation (FCA/ASIC) provide superior Negative Balance Protection, a key requirement for avoiding Gharar.

- Funding Integrity: Shariah prohibits funding accounts with interest-bearing credit lines; use **Debit Cards** or **Bank Transfers** only to maintain capital purity.

See Also: For a technical understanding of the mechanics you are activating, audit our guides on What is an Islamic Account? and the Behind-the-Scenes Liquidity Audit.

Step 1: The Pre-Application Check (Selecting the Forensic Broker)

You cannot open a compliant account with a non-compliant broker. Before you hand over your personal data, you must perform a Pre-Application Audit of the broker’s “Account Specifications” sheet. In 2026, many unregulated brokers use the “Islamic” label as a marketing hook while hiding debt traps in the fine print. As an auditor, I look for **Shariah Certification** from recognized boards like AAOIFI or internal Shariah advisors.

The Forensic Audit Criteria:

- Top-Tier Regulation: Ensure the broker is licensed by an authority that mandates **Segregated Funds** and **Negative Balance Protection** (e.g., **FCA**, **ASIC**, or **CySEC**). Check the FCA Register to verify they aren’t clones.

- Swap-Free Duration: Does the status expire after 5 or 7 days? According to AAOIFI standards, if the status is temporary, the contract contains a future usury clause, making it problematic for **Swing Trading**.

- Hidden Fee Analysis: Look for “Daily Admin Fees” that replace interest. If the fee scales per night, it is **Riba in disguise**. A true Ujrah (Service Fee) must be fixed.

Forensic Audit: Manual vs. Automated Sharia Activation

The Auditor’s Note: In 2026, elite brokers utilize Algorithmic Geo-Fencing. For residents of Muslim-majority regions (e.g., GCC, Pakistan, Malaysia), the “Islamic” status is often hard-coded into the onboarding journey. However, never assume automation is perfection. Even if your account is “Auto-Islamic,” you must still execute the Step 6 Terminal Audit to verify the server-side logic matches the marketing claim.

We have pre-vetted providers who pass these technical checks in our Audit of the Top Islamic Forex Brokers.

The Shariah Governance Audit

Before proceeding, a forensic audit requires checking the **Shariah Governance** structure of the broker. A “Halal” label on a website is marketing; a **Shariah Supervisory Board (SSB)** is governance. In 2026, the gold standard is for a broker to provide an annual audit report or a *Fatwa* certificate specifically for their Islamic account structure. If the broker is a “market maker,” they must demonstrate that their Price Feed Transparency is audited to prevent Ghish (fraud) or excessive Gharar (uncertainty).

Step 2: The Application Process (Avoiding the Interim Riba Risk)

When learning how to open an Islamic Forex account, the technical reality is that most brokers do not have a dedicated “Open Islamic Account” button on their homepage. You usually enter the system through a standard gateway. This creates a “Dangerous Transition” phase where your capital is legally subject to interest until the swap-free flag is manually applied by a human operator.

The Forensic Protocol:

- Register for a Standard Raw or ECN Account. ECN is preferred by auditors as it provides direct market access (DMA) without price manipulation (Gharar).

- Complete the **KYC (Know Your Customer)** process by uploading your Passport and Utility Bill. Forensically, this establishes the **Amanah** (Trust) relationship.

- CRITICAL AUDIT STEP: Do not deposit any funds at this stage. Your account is currently in a Default Interest-Bearing State. If you fund it now, your money is sitting in a usurious environment, and you may accidentally earn interest on your balance.

Step 3: The “Compliance Trigger” (Executing the Request Script)

Because the “Swap-Free” setting is a technical override on the broker’s server, you must manually trigger the contract change. This ensures your account adheres to the 4 Conditions That Make a Forex Trade Halal. You must create a permanent Legal Paper Trail by sending a formal request. In 2026, this is increasingly handled via secure portals, but a direct email to the Onboarding Team remains the gold standard for auditability.

Formal Auditor’s Script for Swap-Free Activation:

Subject: Formal Request for Islamic (Swap-Free) Account Status – [Account ID]

Body: “I have registered account number [Insert Number]. Based on my adherence to Shariah principles, I formally request that this account be converted to ‘Swap-Free’ status immediately. Please confirm that all interest calculations (Swaps) have been disabled and that no time-based handling fees mimicking interest will be applied. I will not fund this account until written confirmation of this contractual change is received.”

This script serves as your Forensic Evidence if the broker ever tries to retroactively charge interest—a common issue in the industry known as “Interest Clawback.” By stating you won’t fund until confirmed, you protect the purity of your Wadi’ah (Deposit).

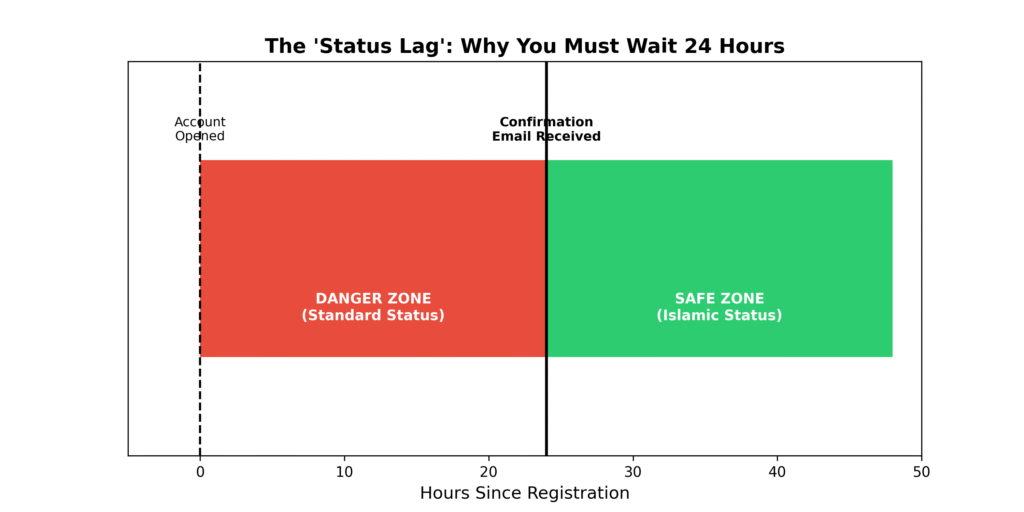

Step 4: The “Danger Zone” (Server-Side Syncing & Tom-Next Audit)

This is the failure point for 90% of traders. There is a **”Status Lag”** between the broker’s support staff saying “It’s done” and the server actually updating your account parameters. In the backend, the server must change your **Swap Profile** from “Standard” to “Islamic” within the bridge software.

The Auditor’s Rule: Do not trade until the rollover hour (5:00 PM EST) has passed at least once after your confirmation. This ensures the server logic has fully cycled through a Tom-Next rollover. Funding before this confirmation is complete constitutes a violation of **Gharar** (Uncertainty), as you are trading without knowing if the contract is Halal or Haram at that specific millisecond.

The MT4/MT5 Server-Sync Audit

Technical Reality: The “Status Lag” occurs because the broker’s CRM (where you see ‘Islamic’) must sync with the trading server (where the swaps are charged). Forensically, these are two different databases. A support agent might mark you as “Swap-Free” in the CRM, but if the server sync fails, you will still be charged. This is why the Rollover Hour (5:00 PM EST) is your clinical test. If you see a $0.01 charge, the sync failed, and the contract remains usurious.

Step 5: The Funding & Wealth Audit (Maintaining Capital Purity)

In 2026, Shariah compliance extends to the origin of your capital. You must ensure your funding method is free of **Riba**. Most brokers offer dozens of methods, but forensically, only a few are compliant for a professional Islamic trader.

- Avoid Credit Cards: Using a credit card to fund an investment involves borrowing on interest. Even if you pay the balance instantly, you are utilizing a usurious financial facility to trade. This pollutes the **Amanah** (Trust) of your capital and introduces a debt-based risk that contradicts Musharakah principles.

- The Preferred Protocol: Use **Bank Wire Transfers** or **Debit Cards** (linked to non-interest checking accounts). This ensures the capital you risk is 100% your own (Equity), which is a requirement for a valid commercial transaction (Tijarah).

Be prepared for the **”Source of Wealth”** audit. Regulated brokers will ask for proof of where your money came from (e.g., salary, business profit). Providing this transparently is a requirement of the **Wadi’ah** (Safekeeping) relationship between you and the broker. It also ensures you aren’t trading with **Haram Wealth** (Mal Haram).

Capital Origin: The Fractional Reserve Reality Check

The Hardest Truth: While we prioritize Debit Cards to avoid personal interest-based debt, you must acknowledge that modern banks use your deposits for fractional-reserve lending. Forensically, your “Pure Equity” is sitting in a Riba-based system until it reaches the broker. To maintain spiritual integrity, a professional trader should perform Monthly Interest Purification, donating a calculated portion of their capital’s “idle bank interest” to charity.

The Shariah Jurisdictional Audit

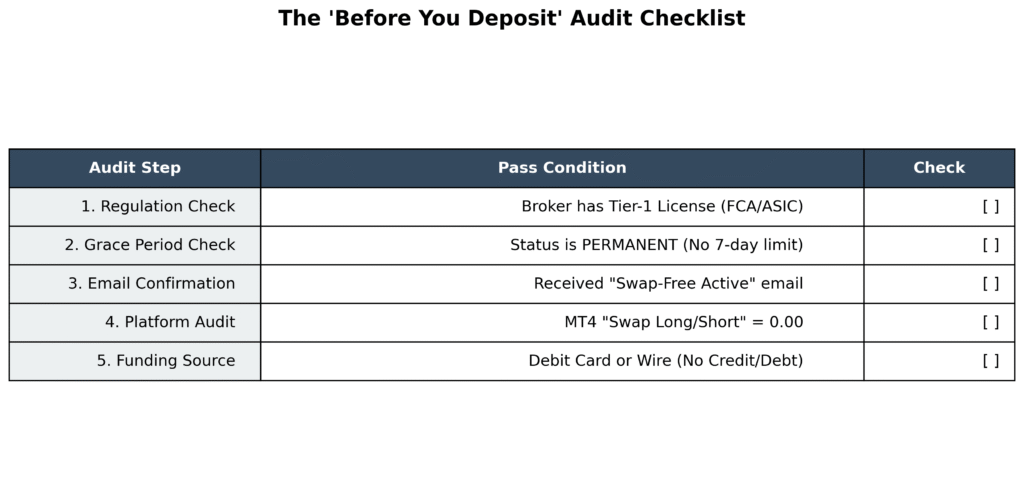

We must address where your account is legally “domiciled.” In 2026, many brokers use offshore subsidiaries (e.g., St. Vincent, Seychelles) to offer higher leverage. However, from a forensic perspective, these jurisdictions often lack the **Negative Balance Protection** and **Investor Compensation Schemes** found in Tier 1 regions. Trading without these protections increases Gharar to a level that some Shariah boards find impermissible. Whenever possible, open your Islamic account under a **Tier 1 Regulator** (FCA, ASIC, CySEC) to ensure your Amanah is legally protected.

The Contract Review: The Terminal Spec Audit

Before you place your first trade, you must perform a Technical Spec Audit inside your MetaTrader 4 or 5 terminal. This is the only way to verify that the broker’s server is actually honoring your request. This is the “Hard Proof” of compliance.

- Open your terminal and right-click on your currency pair (e.g., GBP/USD).

- Select **Specification**.

- Scroll down to the “Swap Long” and “Swap Short” fields.

- The Forensic Requirement: Both fields must be 0.00. If you see negative or positive numbers, your account is **NOT Swap-Free**, and any trade you open will involve Riba.

If you see a value here, do not trade. Contact support immediately and cite your earlier “Compliance Trigger” request. This vigilance is the essence of **Halal Risk Management**. You are auditing the broker’s Wakala (Agency) performance.

Forensic Matrix: Onboarding Compliance Comparison

| Marker | Standard “Marketing” Route | Forensic “Auditor” Route |

| Status Check | Assumed active upon click | Verified via server-side email |

| Funding | Credit card (Riba debt risk) | Direct Debit (Pure Equity) |

| Audit Tool | None (Trust the broker) | Terminal Spec Audit (0.00 swap) |

| Legal Link | None | Signed Wakala/Islamic Agreement |

Frequently Asked Questions

What documents are required to open an Islamic account?

Standard **KYC** documents (Passport/ID and Utility Bill) are mandatory. Additionally, in 2026, many top-tier brokers require a signed **Islamic Declaration Form**. If you live in a non-Muslim majority country, you may need to provide a **Proof of Faith** document (e.g., from a local mosque) to prevent arbitrage abuse of the swap-free privilege.

How long does it take to activate Swap-Free status?

While a standard account opens in minutes, the **Islamic conversion** typically takes 1 to 2 business days. This delay is due to the manual back-office audit and the server-side update required to change your “Swap Profile.” Never fund or trade before the written confirmation arrives.

Can I use a Credit Card to fund my Islamic account?

Technically yes, but forensically no. Credit cards are interest-bearing debt instruments. Using one to fund a Sharia-compliant account creates a **Shariah conflict**. It is highly recommended to use **Debit Cards** or **Local Bank Transfers** to maintain the purity of your capital origins.

Is there a minimum deposit for Islamic accounts?

Yes. Many brokers reserve their “Unlimited Swap-Free” facilities for accounts with a higher minimum deposit (e.g., $1,000+). Accounts with lower balances are often restricted to a 7-day grace period, which is a major **disadvantage** to look out for.

Can I convert an existing Standard account to Islamic?

Yes, but you must close all open trades first. You cannot convert an account while it has active interest-bearing positions. Once closed, you must follow Step 3 of our protocol to request the conversion and wait for confirmation.

Do Islamic accounts require a special platform?

No. You can use **MetaTrader 4**, **MetaTrader 5**, or **cTrader**. The “Islamic” status is a property of the server-side account ID, not the software itself. However, only MT4/MT5 allows you to perform the “Technical Spec Audit” described above.

Does opening an Islamic account affect my spreads?

In many cases, yes. To recover the “lost” swap revenue, brokers may widen the spreads. This is a transparent commercial cost (**Ujrah**) and is permissible as long as it is not predatory. Always check our Hidden Fees Audit before signing up.

What is a “Swap-Free Agreement Form”?

This is a legal document provided by the broker where you declare that your request for a swap-free account is based on religious adherence. Signing this creates the **Forensic Paper Trail** needed to hold the broker accountable to Sharia standards in the event of a dispute.

How can I verify if my funds are segregated?

Audit the broker’s **Legal Documents** (Client Agreement). It should explicitly state that client funds are held in a separate bank account from the broker’s operational funds. In 2026, look for brokers that use Islamic Bank Custody for even higher compliance.

Why was my Islamic account request rejected?

Common reasons include: 1) Living in a country where the broker is not licensed, 2) Existing open trades on a standard account, or 3) Suspected arbitrage activity. If rejected, audit your account status and re-apply after closing all trades.

The “Before You Deposit” Checklist

Do not risk a single dollar of your hard-earned wealth until you pass this final gatekeeper audit. Vigilance in onboarding is the only way to ensure your trading remains **Halal** from the very first pip.

Conclusion: The Verdict

Learning how to open an Islamic Forex account correctly is a continuous process of verification, not a one-time administrative chore. By following this 5-step forensic protocol, you ensure that your trading foundation is built on **Tijarah** (Trade) rather than **Riba** (Usury). Once your account is technically verified as 0.00 swap and funded via non-interest sources, you can apply Halal Trading Strategies with spiritual and financial confidence.

Your Next Step: Do not settle for an unverified account. Start Step 1 today by selecting a broker that passes our technical audit. Read the 2026 Forensic Audit of the Best Islamic Forex Brokers.