Is Forex Swap Haram? The Forensic 2026 Audit of Riba al-Nasiah

Is Forex swap Haram? Yes, the overnight swap is generally considered Haram because it is mathematically derived from the Interest Rate Differential (IRD) between two currencies. In financial auditing, a swap is a charge for the extension of a loan (rollover) past the 5:00 PM EST market close. Because this fee is calculated based on Central Bank interest rates and the duration of the debt, it fits the strict Sharia definition of Riba al-Nasiah (interest of delay). To be permissible, a trade must be executed on a Swap-Free basis that eliminates all time-value-of-money premiums.

For the Muslim trader, the global Forex market presents a unique ethical challenge. While the act of exchanging one currency for another is generally permissible under specific conditions, the mechanism of holding a trade open overnight introduces a hidden financial contract. This contract is the Overnight Swap. Many traders ask: Is Forex swap Haram? They often view it merely as a broker’s service fee. However, when we perform a forensic audit of the financial engineering behind these charges, the reality is different. The “Swap” is not a fee for service. It is a calculation based entirely on interest rate differentials, making it a critical issue for those avoiding Riba (usury).

As a Chartered Certified Accountant (ACCA) with over 19 years of experience in auditing complex financial ledgers, I approach this question with technical rigor. In my professional career, I have seen how brokers “rebrand” interest to appeal to the Islamic market. This guide strips away the marketing jargon to analyze the technical mechanics of the swap, the mathematical proof of its link to Riba, and the specific Sharia rulings that classify it as impermissible in conventional formats.

Key Takeaways: The Auditor’s Summary

- The Mechanism: Swaps are triggered by the “Tom-Next” rollover process, which effectively extends an interest-bearing loan for another 24 hours.

- The Math: The swap rate is derived directly from Central Bank Interest Rates (Interest A minus Interest B) and interbank indices like SOFR.

- The Ruling: Because it is a charge for the delay in settlement, it falls under Riba al-Nasiah (Interest on Delay) and violates the rule of Yadan bi Yad.

- The Solution: Utilizing a verified Swap-Free Account or adopting Intraday Trading (closing before 5:00 PM EST) avoids the swap event entirely.

Forensic Context: This guide is Part 6 of our Halal Trading Silo. For a technical deep dive into related topics, audit our guides on What is Riba?, the Islamic Ruling on Sarf, and Halal vs. Conventional Trading.

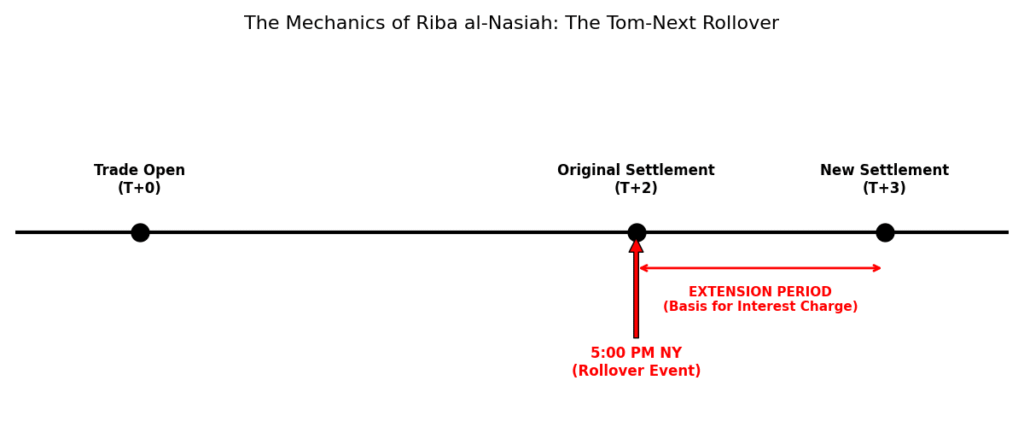

What Actually Is an Overnight Swap? (The Tom-Next Mechanic)

To understand why the answer to “Is Forex swap Haram” is “Yes,” you must first understand the invisible machinery of the Forex market. When you trade a currency pair, you are entering a Spot Contract. In the professional interbank market, spot trades settle in two days (T+2). If you buy EUR/USD on Monday, you are technically obligated to settle the trade—meaning you pay Dollars and receive Euros—on Wednesday.

However, retail CFD traders do not want physical delivery of currency. They only want to speculate on the price movement. To prevent physical delivery, the broker must “roll over” your position to the next settlement date. If you hold a trade past 5:00 PM New York time (the end of the trading day), your broker closes your current T+2 contract and simultaneously opens a new T+3 contract. This process is known in banking as Tom-Next (Tomorrow-Next Day).

This rollover is not free. Since you are trading on financial leverage (borrowed money), keeping the position open requires extending the loan for another 24 hours. The cost (or rebate) for this extension is the Swap. Forensically, this is the exact point where “Trade” turns into “Usury” in a conventional account structure.

The Mathematical Proof: Why Swaps Are “Interest” (Riba)

The most common counter-argument used by non-compliant brokers is that the swap is simply a “service charge” or “administration fee.” In financial auditing, we look past labels to the **underlying calculation method**. The value of the swap is not arbitrary. It is derived strictly from the Interest Rate Differential (IRD) between the two currencies in the pair.

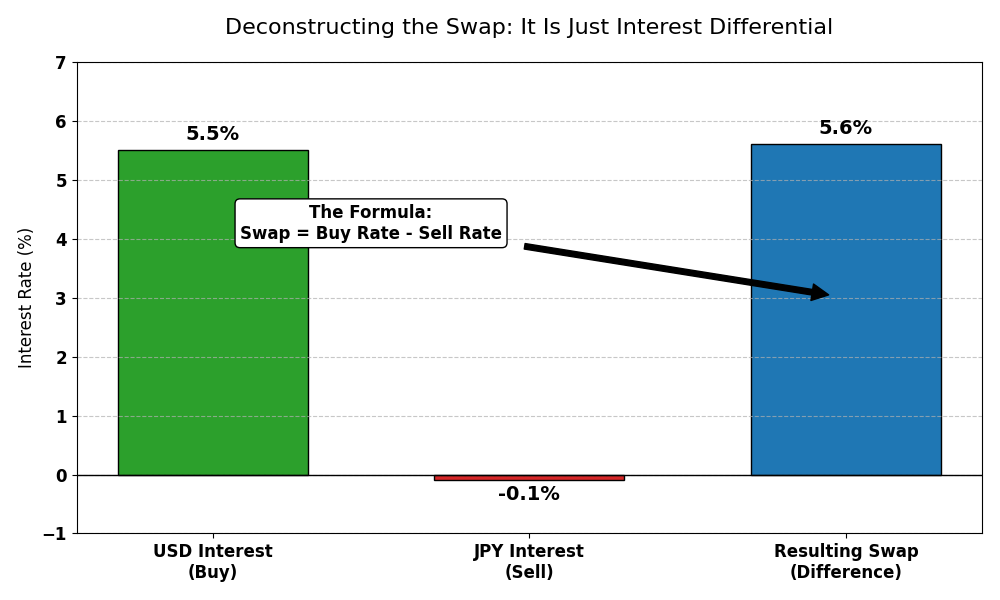

The formula used by the interbank market to calculate the swap is essentially based on the **Net Interest Margin**. Let us look at a concrete forensic example using a high-interest vs. low-interest pair:

- Currency A (USD): Central Bank Rate of 5.50% (The Borrowed Currency)

- Currency B (JPY): Central Bank Rate of 0.10% (The Purchased Currency)

If you are Long (Buying) USD/JPY, you are theoretically earning the high interest on the Dollar and paying the low interest on the Yen. The broker reconciles this gap. Because the input variables for this calculation are **Central Bank Lending Rates** and **SOFR/LIBOR indices**, the output is functionally interest. It is a risk-free return on a loan based purely on time. This fits the classical definition of Riba perfectly, as there is no “work” or “commodity exchange” justifying the fee other than the passage of 24 hours.

Forensic Audit Matrix: Swap vs. Service Fee

| Feature | Overnight Swap (Haram) | Service Fee / Ujrah (Halal) |

| Calculation Method | Derived from Interest Rate Differentials (IRD) | Fixed cost based on operational overhead |

| Market Indexing | Tied to SOFR, EURIBOR, or Fed Funds Rate | Independent of central bank fluctuations |

| Legal Structure | Interest-bearing loan extension | Wakala (Agency) or Service agreement |

| Benefit Logic | Profit from the “Time Value” of money | Profit from “Work” or service provided |

The Theological Verdict: Riba al-Nasiah (Interest on Delay)

In Islamic jurisprudence (Fiqh), the prohibition of Riba is absolute. Specifically regarding Sarf (currency exchange), the rules are strict to prevent “money from generating money” without an underlying trade of assets. **AAOIFI Shariah Standard No. 57** (Gold and Trading in Currencies) explicitly addresses this. The standard stipulates that for a currency trade to be Halal, constructive possession (Qabd) must be immediate.

The Overnight Swap represents a fee paid or received specifically for the delay (Nasiah) in settlement. Standard Sharia rulings define this as:

- Negative Swap: You are paying interest for the privilege of extending the loan period.

- Positive Swap: You are receiving interest for lending your currency to the broker’s pool overnight.

Both scenarios violate the requirement for Yadan bi Yad (hand-to-hand) immediate exchange. Therefore, standard swaps are considered **Riba in disguise**. This is why the answer to “Is Forex swap Haram” remains a definitive “Yes” in the context of standard conventional accounts.

The “Islamic Account” Loophole: Is it Really Halal?

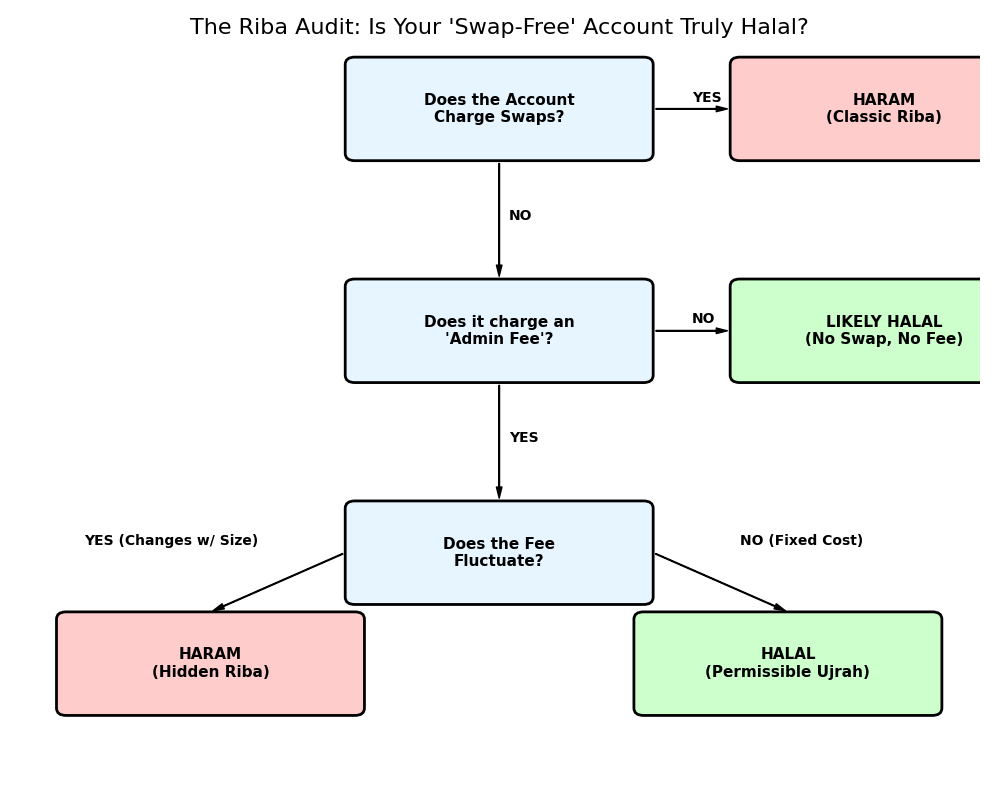

Recognizing this issue, many brokers offer Islamic (Swap-Free) accounts. In these accounts, the swap fee is removed. However, as an auditor, I recommend you audit these accounts with extreme caution. Some brokers replace the Riba-based swap with an “Administration Fee.” You must determine if this is just Riba by another name. Use this forensic checklist:

- Variable Fees: Does the “Admin Fee” change based on the currency pair’s interest rate? If yes, it is Riba.

- Time-Scaling: Does the fee increase every day you hold the trade? A true service fee (**Ujrah**) should be fixed for the work, not a percentage of the loan amount calculated daily.

The Economic Equivalence Audit: Catching Rebranded Riba

The Auditor’s Test: If an “Islamic Admin Fee” equals $10 and the conventional swap would have been $10, we have Economic Equivalence. A true audit asks: “Does the work performed by the broker (Wakala) actually cost more on a Wednesday?” If a broker triples their “Admin Fee” on Wednesdays to match the interbank “Triple Swap,” they are mimicking the interest-bearing calendar. A legitimate service fee must be decoupled from central bank policy. If it mimics the banking calendar, it is Riba rebranded, and the auditor must fail the compliance test.

The Impact of SOFR on Forex Swaps

In 2025 and 2026, the global financial system has shifted significantly toward the **Secured Overnight Financing Rate (SOFR)** as the primary benchmark for USD-based transactions. For the Muslim trader, this change is critical because SOFR is fundamentally a measure of the cost of borrowing cash overnight collateralized by Treasury securities. When a broker calculates a USD-based swap, they are using SOFR as the baseline. Because SOFR is a direct measure of interest-on-debt, any swap linked to it is forensically tied to Riba. This technical link is what many “Sharia-certified” brokers fail to disclose to their clients. My audit methodology requires brokers to decouple their platform fees from these interest-bearing indices to maintain a “Halal” status.

Valid Alternatives for Muslim Traders

If standard swaps are Riba, and some Islamic accounts are questionable, what is the solution? You must either utilize a strictly audited Halal Forex Broker that charges a fixed Ujrah, or adopt an Intraday trading strategy.

- 1. Intraday Trading (The Purest Path): The most secure method is to ensure your trades never trigger the rollover event. By closing all positions before 5:00 PM New York time, the trade settles within the same day (T+0). No rollover occurs, no swap is generated, and the transaction remains compliant with the requirement of immediate settlement.

- 2. Qard Hasan Leverage: Seek brokers that provide leverage as a Qard Hasan (interest-free loan). In this model, the broker makes no profit from the loan itself, only from the transparent commissions on the trade execution. This aligns with the risk-sharing philosophy of **Ghunm bil Ghurm**.

- 3. Physical Settlement: While rare in retail trading, using platforms that allow for true physical delivery of the currency removes the “Tom-Next” requirement entirely.

The Forensic Warning: Systemic Riba Contamination

Adversarial Audit Note: While the alternatives above (especially Intraday Trading) successfully bypass the Swap contract, a forensic auditor must acknowledge the Liquidity Origin. In a globalized economy, the price feeds and liquidity bridges provided by Tier-1 banks are “powered” by interest-bearing capital.

Even if your individual trade never triggers a rollover, you are a participant in a market where the baseline indices (like SOFR) are derived from usury. In Sharia forensics, this is known as the “Dust of Riba.” While it does not render your specific trade Haram, it necessitates a higher level of Spiritual Risk Management. We recommend that a portion of all trading profits be set aside for interest purification (charitable donation) to offset any indirect benefits gained from this systemic contamination.

Forensic Summary: Tom-Next vs. Compliance

The auditor’s goal is to ensure that the “Contract of Sale” (Trade) is not polluted by the “Contract of Loan” (Swap). In 2026, AI-driven auditing tools have made it easier to track these micro-transactions. If your broker’s ledger shows a charge that fluctuates with **Central Bank Policy Rates**, you are engaging in a usurious contract, regardless of the account name.

Frequently Asked Questions

What exactly is an Overnight Swap?

**An overnight swap** is a fee paid or received for rolling over a Forex trade past 5:00 PM EST. It is the cost of extending a leveraged loan from the original settlement date (T+2) to the next day (T+3). In banking, this is known as a **Tom-Next rollover**.

Why are Forex swaps considered Riba (Haram)?

**Forex swaps** are Haram because they are derived from central bank interest differentials. Forensically, a swap is an interest-bearing premium charged for the delay in repayment (**Riba al-Nasiah**), making it a usurious increase on a loan.

Are “Swap-Free” Islamic accounts always Halal?

Not always. You must audit the **Administration Fee**. If the fee fluctuates with interest rates or scales daily based on loan size, it is simply **Riba in disguise**. A truly Halal account uses a fixed service fee (**Ujrah**) for agency work (**Wakala**).

How can I avoid swaps entirely without an Islamic account?

The only 100% secure method is **Intraday Trading**. If you close all positions before the 5:00 PM EST rollover window, no interest is triggered, keeping your capital Riba-free and your trade within the **T+0 settlement** window.

Is a Positive Swap Halal if the broker pays me?

No. **Positive Swaps** are unearned interest income. Receiving interest is just as prohibited as paying it in Sharia. Any such gain must be purified by donation to charity to maintain the integrity of your capital.

Does Scalping avoid Riba?

Yes. **Scalping** involves opening and closing trades within minutes. Since these trades never reach the daily rollover time, they are never subject to **overnight swaps**, making them forensically Halal regarding Riba.

What is “Tom-Next” in Forex?

**Tom-Next** (Tomorrow-Next Day) is the banking mechanic used to roll over positions to avoid physical delivery. Because it is a contract to defer settlement for a price (interest), it is the primary source of Riba in conventional trading.

What is the difference between Riba al-Nasiah and Riba al-Fadl?

**Riba al-Nasiah** is interest charged for a delay in repayment, which is the swap. **Riba al-Fadl** is an excess in the exchange of same-item commodities. Forex traders primarily encounter Riba al-Nasiah during the rollover phase.

Can I use a “Margin Account” without incurring Riba?

Only if that margin is provided as a **Swap-Free** facility. A standard margin account is an interest-bearing loan account. You must switch to a certified **Islamic Margin** structure to remain compliant.

Is the “Forex Spread” considered Riba?

No. **The Forex Spread** is the difference between the bid and ask price. It is a transparent transaction cost and is permissible as a legitimate business profit for the broker facilitating the exchange.

Conclusion: The Final Verdict

So, is Forex swap Haram? The answer from a forensic auditing perspective is yes. The Overnight Swap is not a random service fee; it is a precise financial calculation based on the time-value of money and interest rate differentials. Because it is a charge for the extension of a loan period, it falls squarely under the definition of Riba al-Nasiah. For the Muslim trader, the path forward is clear. You must either utilize a strictly audited Halal Forex Broker that charges a fixed Ujrah, or adopt an Intraday trading strategy that avoids the swap mechanism entirely. Ignoring the mechanics does not remove the reality of the interest charge or the risk of Gharar (excessive uncertainty) in your contract.

Your Next Step: Verify your broker’s rollover policy today. I have forensically audited the top platforms to identify those that provide true Swap-Free execution without hidden Riba fees. Read the 2026 Forensic Audit of the Top 5 Islamic Brokers.